Compound Interest Calculator

There is a reason compound interest is called the most powerful force in personal finance. Our calculator lets you see it in action: enter your starting amount, how much you can add each month, your expected return, and for how long — and watch your money grow in real time, with a chart and a period-by-period table.

Fill in the fields above, hit Calculate, and explore your results.

What Is Compound Interest?

Compound interest is the process by which the returns on an investment generate their own returns. In other words, you earn interest on your interest — and that makes the growth exponential rather than linear.

With simple interest, your return is always calculated on the original principal. With compound interest, your return is calculated on the full accumulated balance — including all the interest earned so far. Over long periods, this difference is enormous.

A concrete example:

Say you invest $10,000 at an annual return of 8%.

- With simple interest, after 20 years you would have: $10,000 + ($800 × 20) = $26,000

- With compound interest, after 20 years you would have: $10,000 × (1.08)²⁰ = $46,609.57

That is nearly $21,000 more — from the exact same starting point and the exact same rate. The only difference is that compound interest kept putting previous gains back to work.

How Our Compound Interest Calculator Works

Our tool uses the complete financial formula for investments with recurring monthly contributions. Here is what each input means:

Initial Amount (PV — Present Value): The capital you have available to invest today. This can be zero if you are starting from scratch and relying purely on monthly contributions.

Monthly Contribution (PMT — Payment): The amount you add to your investment each month, on top of the initial amount. Regular contributions have a compounding effect of their own — each new deposit starts earning interest immediately. Over decades, monthly contributions often matter more than the initial amount.

Interest Rate: Your expected annual or monthly return. You can enter either — the calculator converts automatically using exponential equivalence, which is the mathematically correct method (not a simple division by 12).

Time Period: How long you plan to keep the money invested. Time is the single most powerful lever in compound interest. Starting a few years earlier can be worth more than doubling your monthly contribution.

Step-by-Step: How to Use the Calculator

Step 1 — Enter your initial amount: Type in how much you have to invest right now. If you are starting from zero, leave this field blank or enter 0.

Step 2 — Set your monthly contribution: Enter the amount you plan to invest every month. Even small consistent contributions — $50, $100, $200 — produce surprising results over long periods.

Step 3 — Choose your interest rate and type: Enter your expected return and select whether it is annual or monthly. For context: broad stock market index funds have historically returned around 7–10% per year over long periods; high-yield savings accounts currently range from 4–5% annually; and money market accounts or CDs vary by term and institution.

Step 4 — Select your time period: Enter the number of years or months. Run a few scenarios — try 10, 20, and 30 years to see how dramatically time changes the outcome.

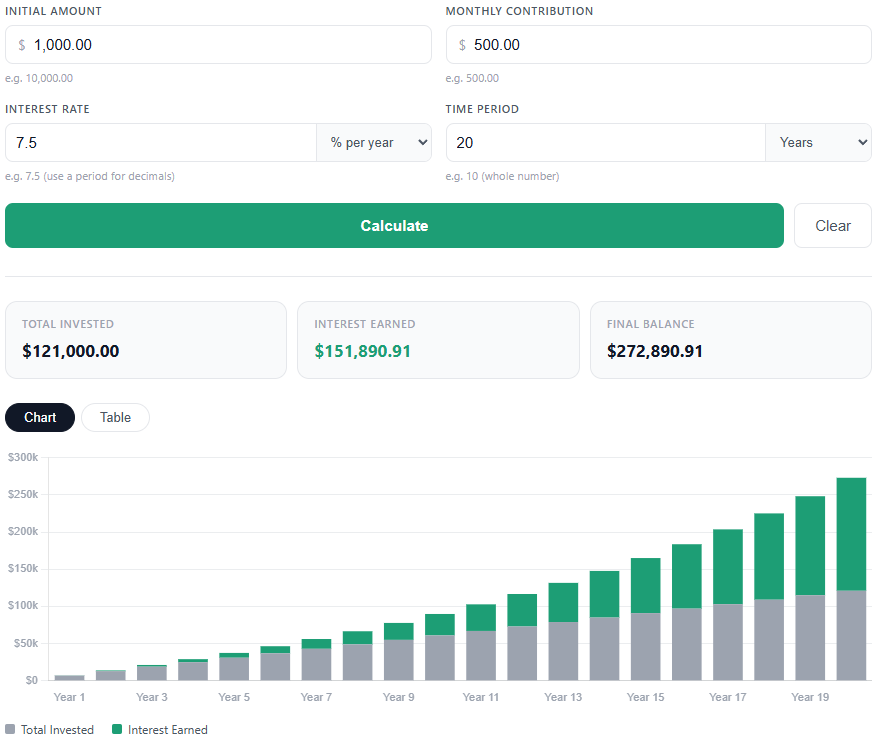

Step 5 — Click Calculate: The calculator displays three key figures:

- Total Invested: the money you personally contributed

- Interest Earned: the growth generated by compounding

- Final Balance: the full amount available at the end of the period

Toggle between the Chart (stacked bars by year or month) and the Table (detailed breakdown for every period) to explore your results from different angles.

The Compound Interest Formula

The base formula for compound interest without contributions is:

A = PV × (1 + r)ⁿ

Where:

- A = Final balance

- PV = Principal (initial investment)

- r = Interest rate per period

- n = Number of periods

When monthly contributions are included, the complete formula is:

A = PV × (1 + r)ⁿ + PMT × [(1 + r)ⁿ – 1] / r

Where PMT is the recurring monthly contribution. This is the formula our calculator applies — the same one used in professional financial analysis and CFA-level coursework.

Annual-to-monthly rate conversion

When you enter an annual rate, the calculator converts it to a monthly rate using:

r_monthly = (1 + r_annual)^(1/12) – 1

This is the exponentially equivalent rate — the mathematically precise method. Many calculators simply divide the annual rate by 12, which introduces a compounding error that grows significantly over long time horizons.

Why Time Is the Most Powerful Variable

The longer your money compounds, the more dramatic the effect. This is not intuitive — our brains tend to think in straight lines, not exponential curves. But the math is unambiguous.

Consider two investors:

- Investor A starts at age 25, invests $300 per month for 15 years at 8% annual return, then stops completely at age 40.

- Investor B starts at age 40, invests $300 per month for 25 years at the same 8% return, continuing all the way to age 65.

Investor B invested for 10 more years and contributed $36,000 more in total. Yet at age 65, Investor A — who stopped investing a quarter century earlier — would still have a larger final balance. The 15 extra years of compounding from age 25 to 40 cannot be made up by simply contributing more later.

This is why the most actionable advice in personal finance is also the most repeated: start as early as you can, even with small amounts.

Recommended Reading

- What is Dollar-Cost Averaging? The Beginner’s Guide

- Mark Tilbury’s Stock Market Crash Strategy: 2026 Wealth Guide

- Warren Buffett’s Portfolio: What Does He Actually Invest In?

- Read more

Compound Interest For You — and Against You

Compounding is a force, not a direction. It amplifies whatever financial position you are already in.

When it works in your favor (investments and savings): In any savings or investment account — a brokerage account, a 401(k), an IRA, a high-yield savings account, or a CD — compound interest grows your balance faster the longer you leave it untouched. Every dollar of gain becomes the foundation for the next round of gains.

When it works against you (debt): In credit card debt, personal loans, or any high-interest borrowing, compounding works in the lender’s favor. A $5,000 credit card balance at 20% APR, left unpaid for 5 years, grows to over $12,000 — without a single new purchase. Understanding this is the first step toward prioritizing high-interest debt repayment before aggressive investing.

What Interest Rate Should You Use?

The right rate to use depends entirely on the type of account or investment you are modeling. Here are common benchmarks as of 2026:

- S&P 500 index funds (historical average): approximately 7–10% per year, before inflation

- High-yield savings accounts: currently around 4–5% annually

- 10-year U.S. Treasury bonds: approximately 4.3–4.6% annually

- Certificates of Deposit (CD): typically 4–5% for 1–5 year terms

- Money market accounts: around 4–5% annually

When using this calculator for long-term planning, it is worth running at least three scenarios: a conservative rate, a moderate rate, and an optimistic rate. The spread between outcomes will show you how sensitive your plan is to return assumptions — and why diversification and consistency matter more than chasing high returns.

Frequently Asked Questions

What is the difference between simple interest and compound interest? Simple interest is calculated only on the original principal — growth is linear. Compound interest is calculated on the full accumulated balance, including all prior interest — growth is exponential. For any investment held longer than a few months, compound interest produces a higher final balance than simple interest at the same rate.

Does compound interest apply to savings accounts? Yes. Any savings account that credits interest to your balance (which is nearly all of them) is using compound interest. The difference between accounts lies in how frequently interest is compounded — daily, monthly, or annually. More frequent compounding results in a slightly higher effective annual yield (APY).

Can I use this calculator to model debt? Yes. Enter the loan or debt amount as the initial amount, the interest rate you are being charged, and the loan term. The final balance will show how much the debt grows if no payments are made — a sobering way to understand the true cost of high-interest borrowing.

Why does the calculator convert annual rate to monthly using a formula instead of dividing by 12? Dividing an annual rate by 12 is a common simplification, but it is mathematically incorrect. A 12% annual rate is not the same as twelve separate 1% monthly rates — because the monthly compounding creates a slightly higher effective annual rate. The correct method is exponential equivalence: r_monthly = (1 + r_annual)^(1/12) – 1. The error from simple division is small in the short term but grows noticeably over 10–30 year projections.

What does “monthly contribution” mean in the calculator? It is the fixed amount you add to the investment at the end of each month, in addition to the initial amount. The calculator assumes consistent contributions throughout the entire period. Even if your actual contributions vary, the tool is useful for modeling a target monthly savings rate and seeing its long-term impact.

More Tools to Help You Plan

SOON

All simulations are for educational and illustrative purposes only and do not represent a guarantee of future returns. Past performance is not indicative of future results. Consult a licensed financial advisor before making investment decisions.